Understanding how loan interest rates work is essential for anyone who borrows money. Whether you’re taking out a personal loan, mortgage, student loan, or business financing, the interest rate directly affects how much you ultimately pay. Many borrowers focus only on the monthly payment, but the real cost of a loan lies in how interest is calculated and applied over time.

In this comprehensive guide, we will break down how loan interest rates function, the factors that influence them, and most importantly, practical strategies to reduce your borrowing costs. By the end of this article, you’ll have the knowledge needed to make smarter financial decisions and potentially save thousands of dollars.

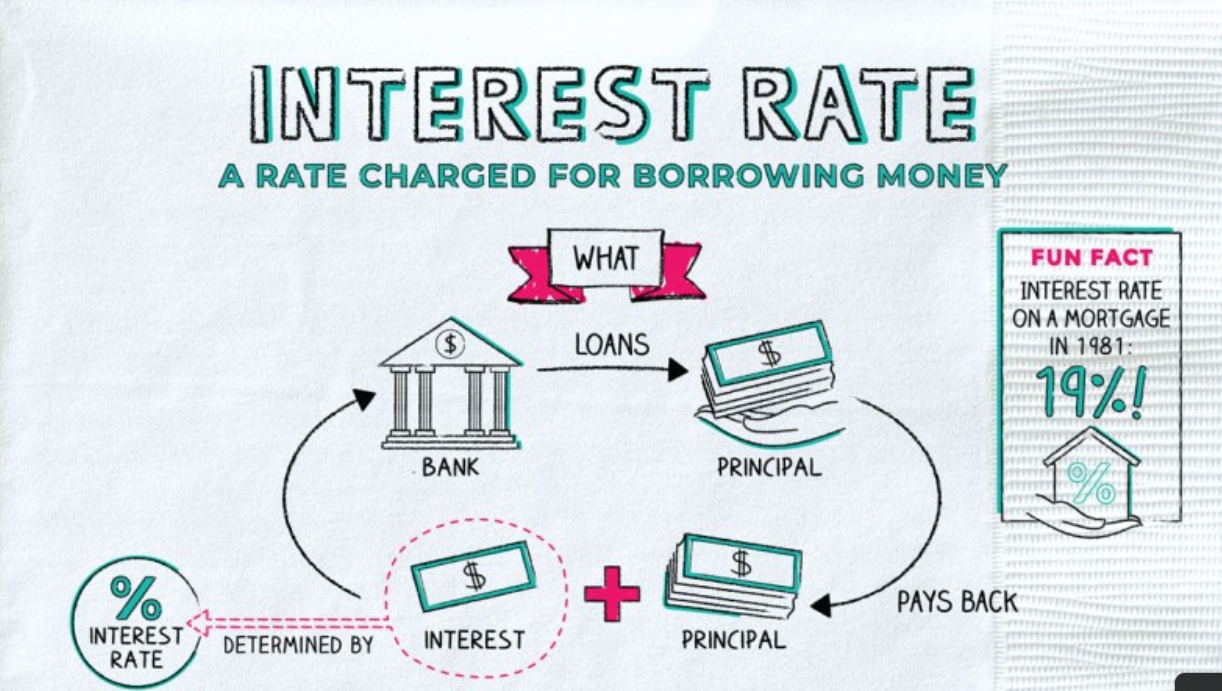

What Is a Loan Interest Rate?

A loan interest rate is the percentage charged by a lender on the amount of money you borrow. It represents the cost of borrowing and is typically expressed as an annual percentage.

For example, if you borrow $10,000 at a 10% annual interest rate, you’ll pay $1,000 in interest per year—assuming simple interest and no repayments during that time.

However, most loans are more complex. Interest is often calculated on a declining balance and may compound over time, which means the actual cost can be higher than expected.

Types of Loan Interest Rates

1. Fixed Interest Rate

A fixed interest rate remains the same throughout the life of the loan. This means your monthly payments stay consistent, making it easier to budget.

Advantages:

- Predictable payments

- Protection from market rate increases

Disadvantages:

- Typically higher initial rate compared to variable loans

- No benefit if market rates decrease

2. Variable Interest Rate

A variable (or adjustable) interest rate can change over time based on market conditions.

Advantages:

- Lower starting rate

- Potential savings if rates decrease

Disadvantages:

- Unpredictable payments

- Risk of rising interest costs

3. Simple Interest vs. Compound Interest

Simple Interest is calculated only on the principal amount.

Compound Interest is calculated on both the principal and accumulated interest.

Most modern loans use compound interest, which can significantly increase the total repayment amount if not managed carefully.

How Interest Is Calculated

Understanding how lenders calculate interest can help you better evaluate loan offers.

Daily Interest Calculation

Some loans calculate interest daily using this formula:

Interest = Principal × Rate ÷ 365

This means the faster you pay down your loan, the less interest you’ll accumulate.

Amortized Loans

Most installment loans (like mortgages or car loans) use amortization. This means:

- Each payment includes both principal and interest

- Early payments are mostly interest

- Later payments go more toward principal

This structure is why paying extra early in the loan term can save significant money.

Factors That Affect Your Interest Rate

1. Credit Score

Your credit score is one of the most important factors. Higher scores indicate lower risk, leading to better interest rates.

2. Loan Term

Shorter loan terms usually have lower interest rates but higher monthly payments.

3. Economic Conditions

Interest rates are influenced by inflation, central bank policies, and overall economic health.

4. Loan Type

Secured loans (backed by collateral) typically have lower rates than unsecured loans.

5. Income and Debt Ratio

Lenders assess your ability to repay. A lower debt-to-income ratio can result in better rates.

APR vs. Interest Rate

Many borrowers confuse APR (Annual Percentage Rate) with the interest rate.

- Interest Rate: Cost of borrowing the principal

- APR: Includes interest plus fees and additional costs

APR gives a more accurate picture of the total loan cost and should always be compared when evaluating offers.

The True Cost of Interest Over Time

Even a small difference in interest rate can have a big impact.

For example:

- A $200,000 loan at 5% vs. 6%

- Over 30 years, that 1% difference could cost tens of thousands of dollars

This is why understanding and negotiating your interest rate is crucial.

How to Reduce Your Loan Interest Costs

Now that you understand how interest works, let’s explore actionable strategies to reduce your costs.

1. Improve Your Credit Score

Before applying for a loan, take steps to improve your credit score:

- Pay bills on time

- Reduce credit card balances

- Avoid new debt inquiries

Even a small improvement can qualify you for a significantly lower rate.

2. Shop Around for Lenders

Different lenders offer different rates. Always compare:

- Banks

- Credit unions

- Online lenders

Getting multiple quotes can help you find the best deal.

3. Choose a Shorter Loan Term

While monthly payments may be higher, shorter terms often come with lower interest rates and less total interest paid.

4. Make Extra Payments

Paying more than the minimum reduces your principal faster, which lowers the interest you pay over time.

Tips:

- Make biweekly payments instead of monthly

- Add extra to your principal whenever possible

5. Refinance Your Loan

Refinancing replaces your current loan with a new one at a lower interest rate.

Best time to refinance:

- When interest rates drop

- When your credit score improves

Be sure to consider fees before refinancing.

6. Use Automatic Payments

Some lenders offer discounts for enrolling in autopay. Even a small rate reduction can lead to noticeable savings over time.

7. Avoid Late Payments

Late payments can result in penalties and higher interest rates. Always pay on time to avoid unnecessary costs.

8. Negotiate Your Rate

Many borrowers don’t realize that interest rates can sometimes be negotiated.

If you have:

- Strong credit

- Stable income

- Competing offers

You may be able to secure a better rate.

9. Make a Larger Down Payment

For loans like mortgages or car loans, a larger down payment reduces the loan amount and may qualify you for a lower interest rate.

10. Understand Loan Fees

Hidden fees can increase your overall cost. Always review:

- Origination fees

- Prepayment penalties

- Closing costs

Choosing a loan with slightly higher interest but lower fees may save money overall.

Common Mistakes to Avoid

Ignoring the APR

Always compare APR, not just the interest rate.

Borrowing More Than Needed

Larger loans mean more interest paid over time.

Focusing Only on Monthly Payments

Lower monthly payments often mean longer terms and higher total interest.

Not Reading the Fine Print

Loan terms can include clauses that increase costs unexpectedly.

Advanced Strategies for Reducing Interest

Debt Snowball vs. Debt Avalanche

- Snowball Method: Pay off smallest debts first

- Avalanche Method: Pay off highest interest rates first

The avalanche method saves more on interest, while the snowball method provides psychological motivation.

Consolidation Loans

Combining multiple debts into one loan with a lower interest rate can simplify payments and reduce overall costs.

Balance Transfers

For credit card debt, transferring balances to a lower-rate card can reduce interest—especially if there’s a 0% introductory offer.

Why Timing Matters

Interest rates fluctuate based on economic conditions. Borrowing when rates are low can significantly reduce costs.

Keep an eye on:

- Central bank announcements

- Inflation trends

- Market forecasts

Timing your loan strategically can lead to major savings.

The Role of Financial Discipline

Even with the best interest rate, poor financial habits can lead to unnecessary costs.

Key habits:

- Budgeting consistently

- Avoiding unnecessary debt

- Tracking expenses

- Building an emergency fund

Financial discipline ensures you maximize the benefits of a good loan.

Conclusion

Loan interest rates play a critical role in determining the total cost of borrowing. By understanding how they work—from calculation methods to influencing factors—you can make more informed decisions and avoid costly mistakes.

Reducing your loan costs isn’t just about finding the lowest rate. It involves improving your financial profile, choosing the right loan structure, and actively managing your debt.

Whether you’re planning to take out a loan or already have one, applying the strategies outlined in this guide can help you save money, reduce stress, and achieve your financial goals faster.

Take control of your borrowing today—because even small changes in interest rates can lead to big savings over time.